Accurate measurement is hard.

That's what makes it an edge.

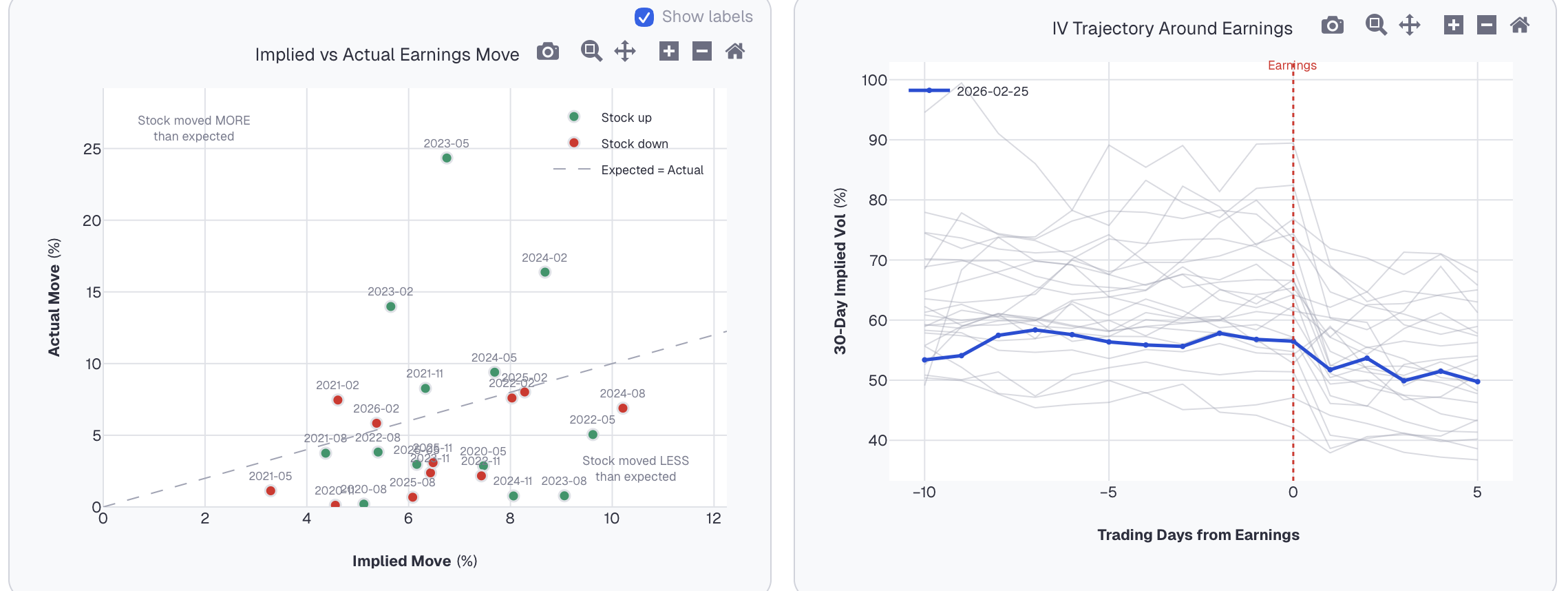

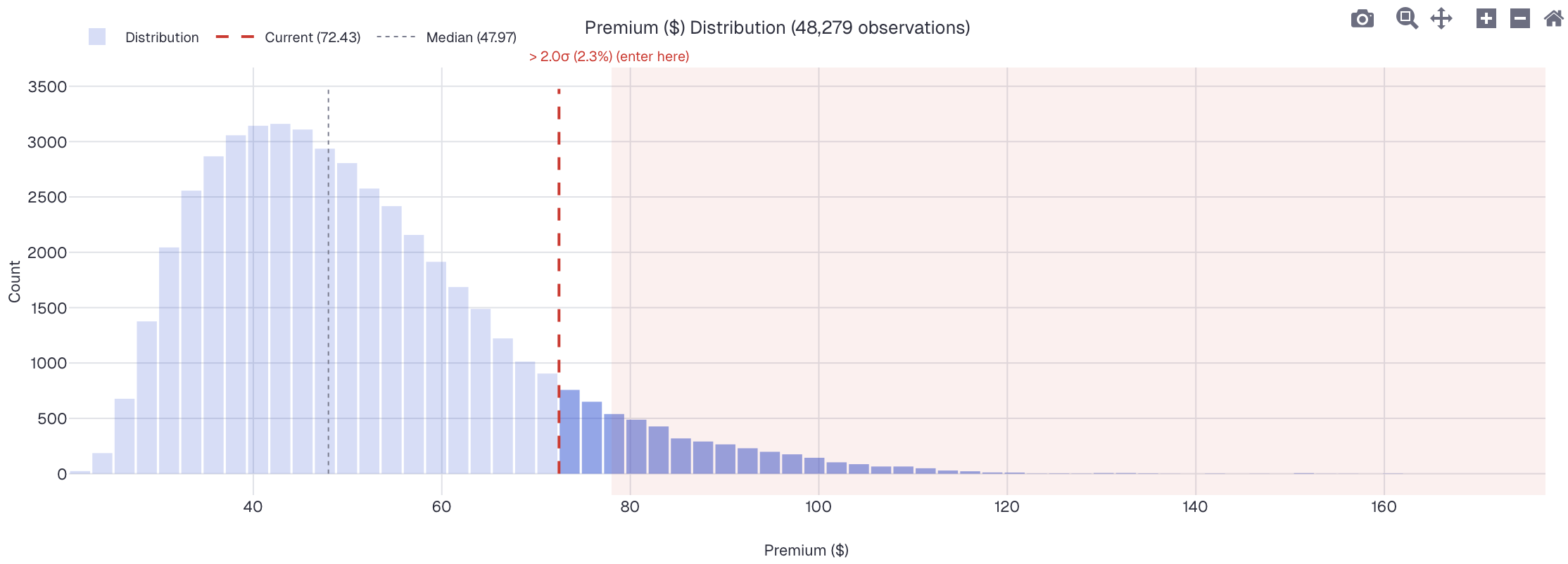

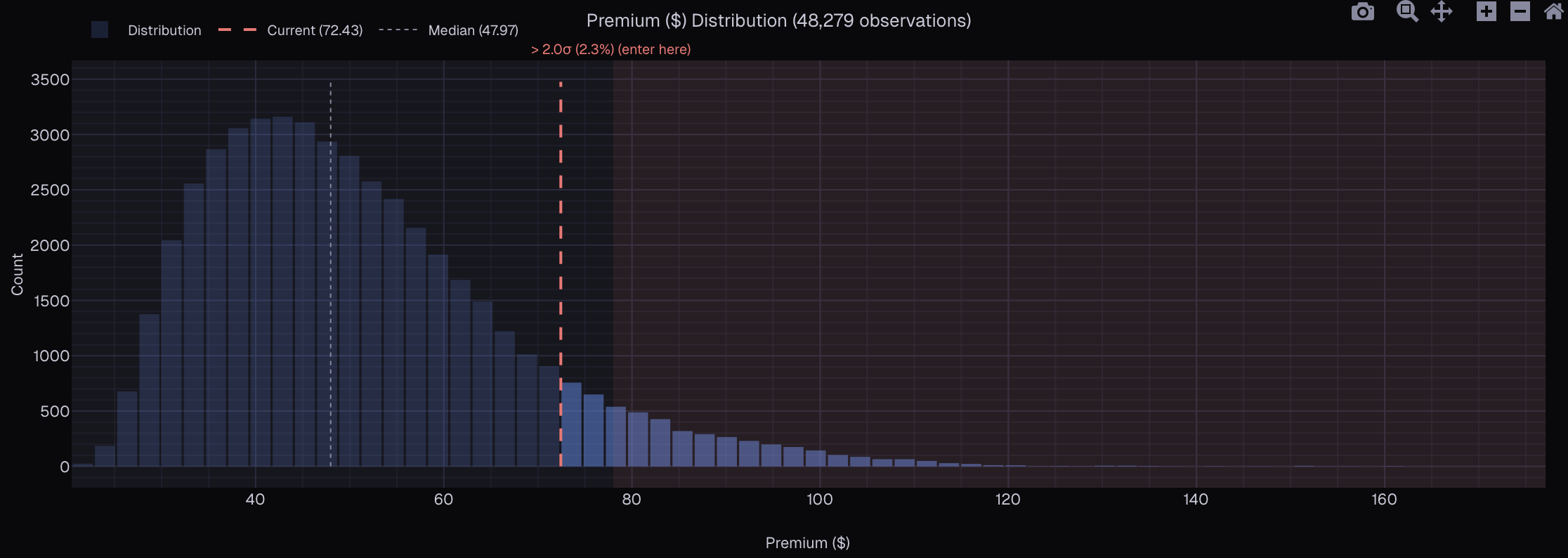

Accurate measurement based on institutional-grade vol pricing, systematic research, and historical simulation — built for options traders who care about getting the details right.