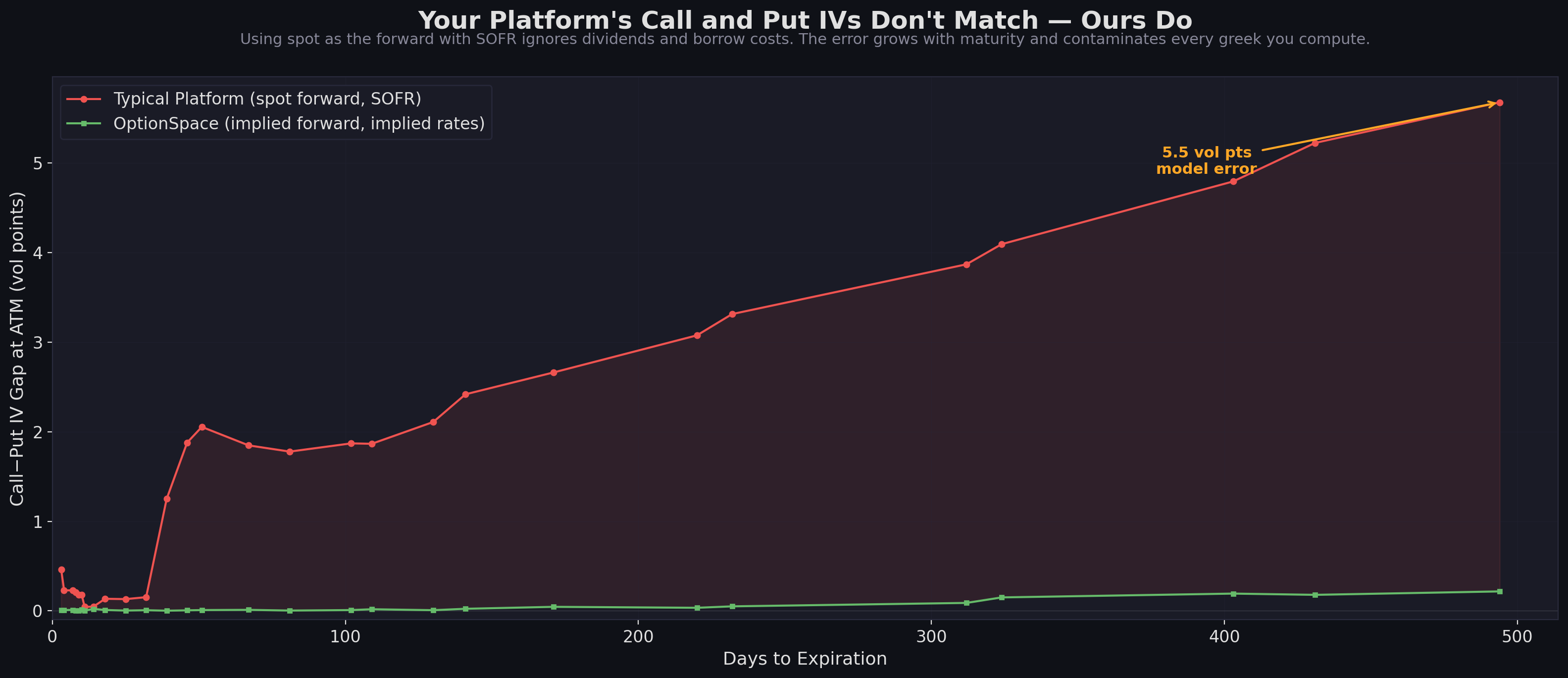

1 Day to Expiry: The Error Is Already There

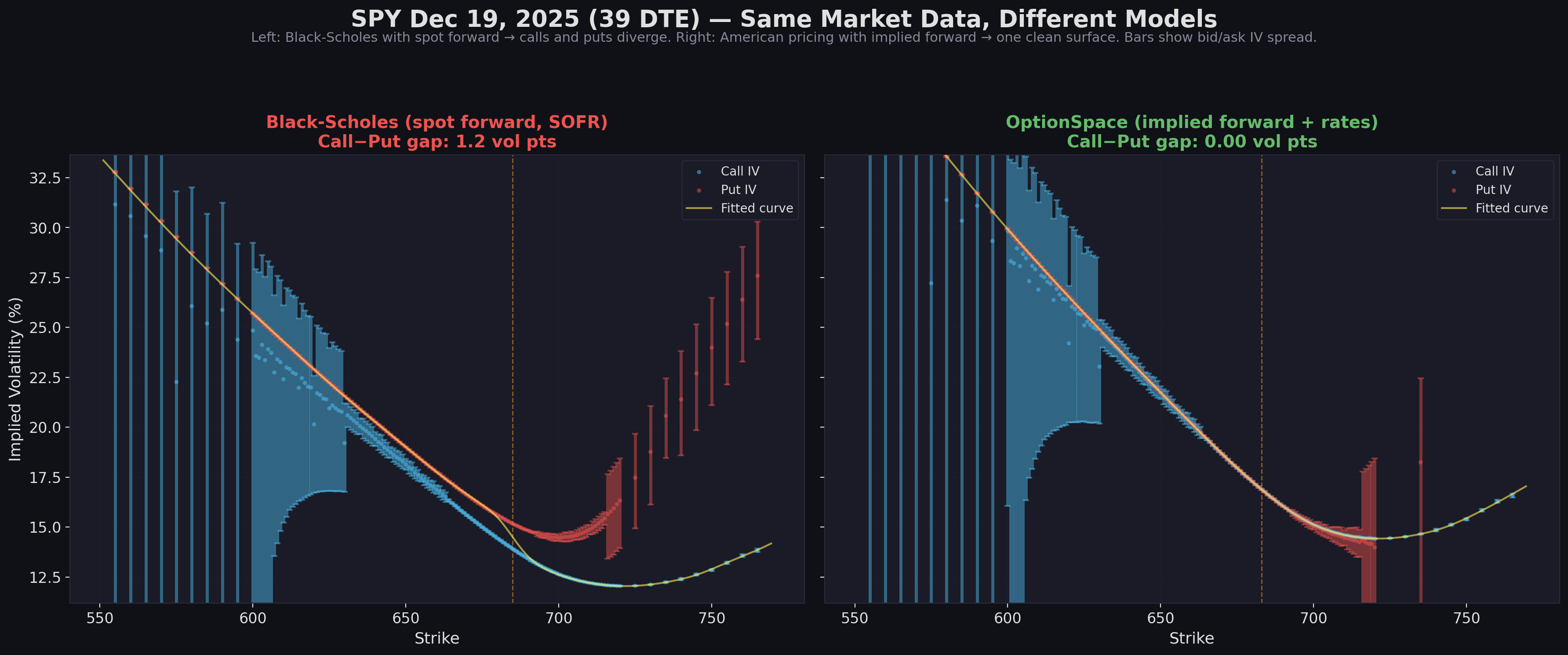

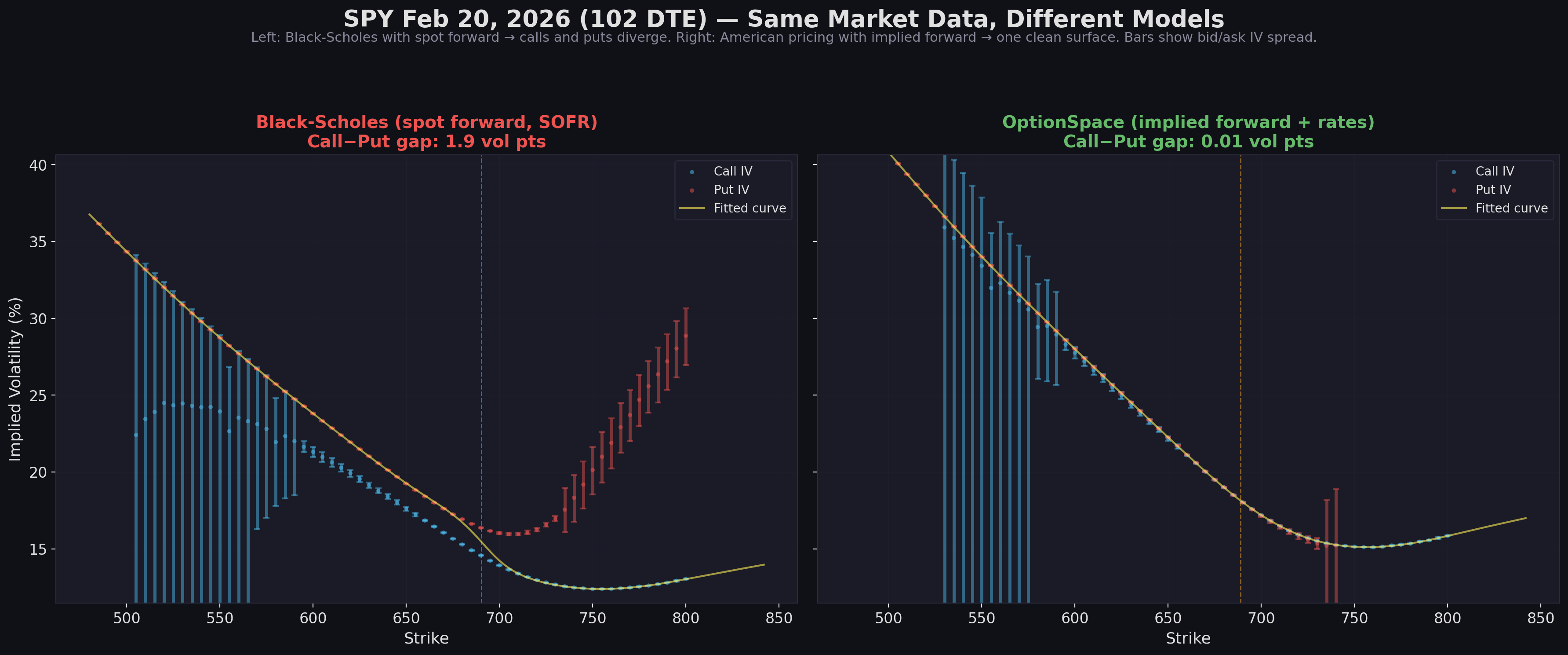

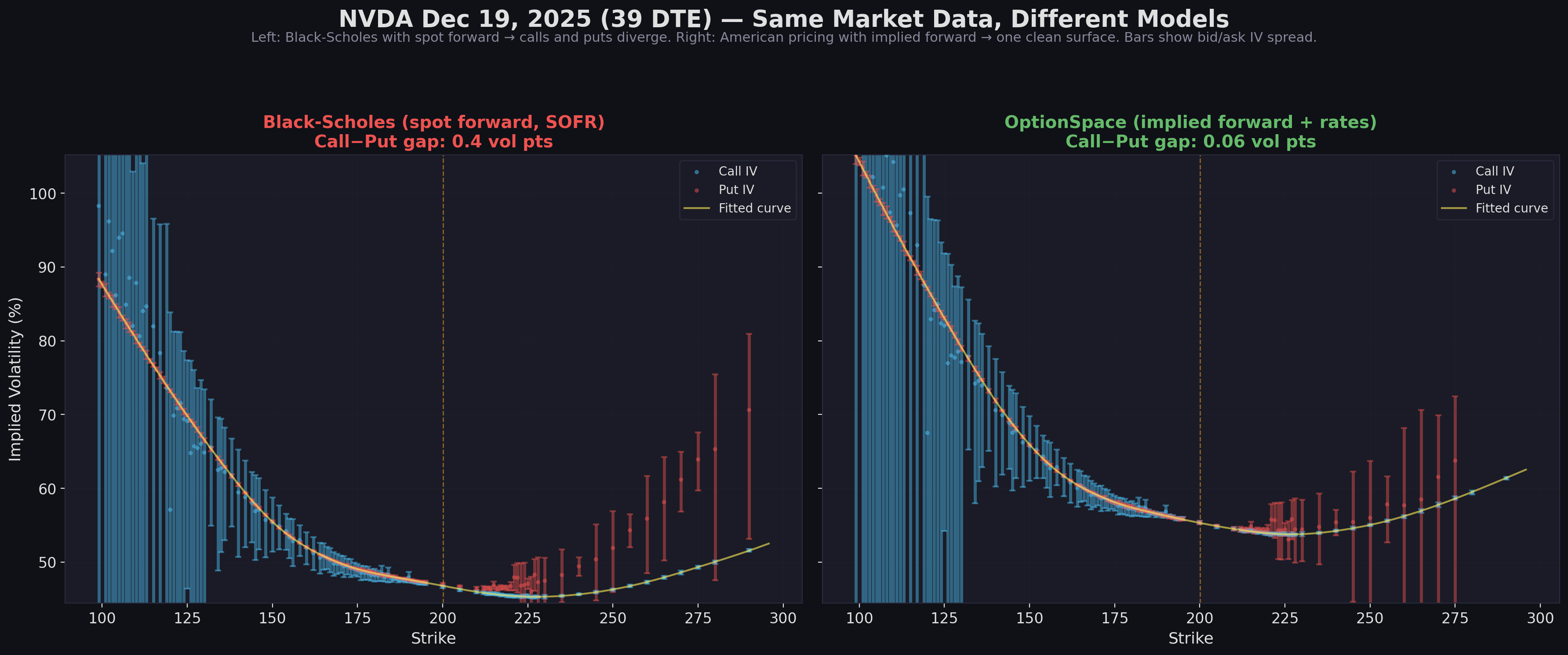

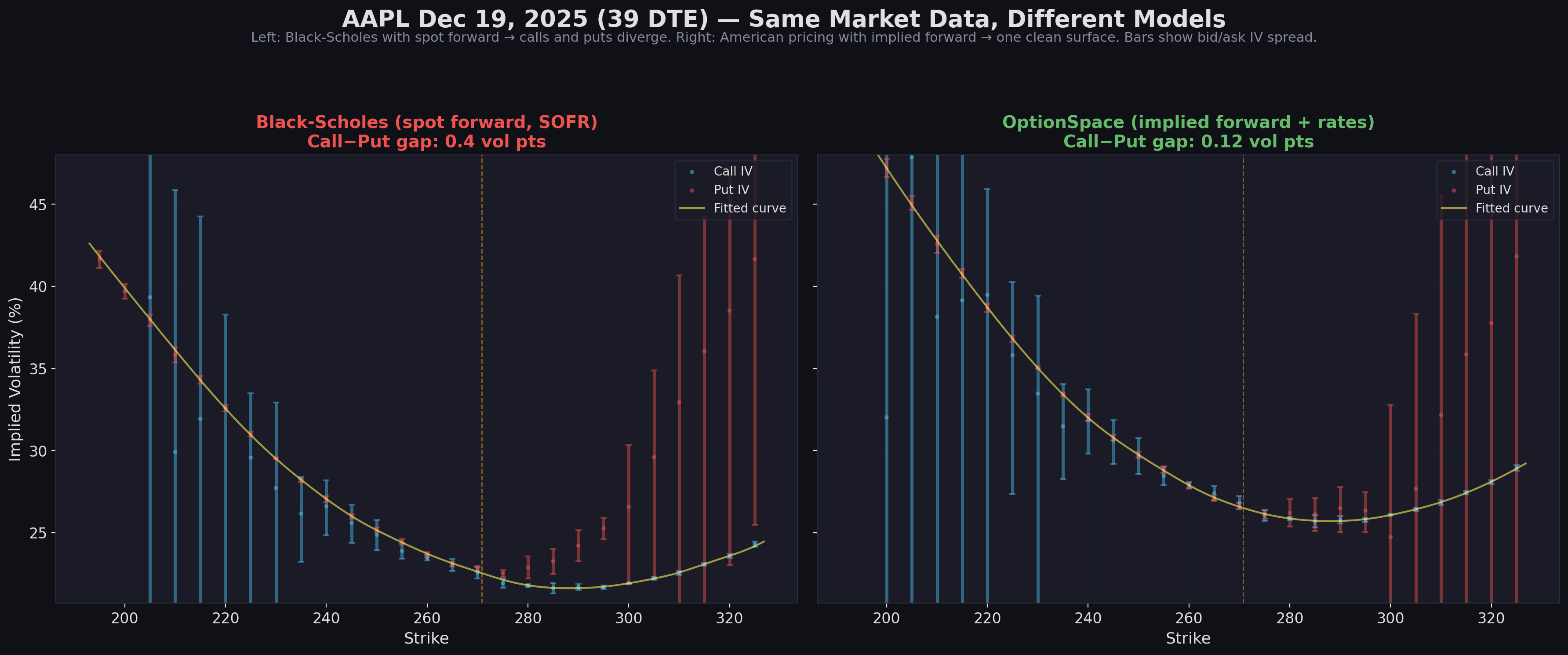

Even for a 1 DTE option, using spot as the forward with a flat rate creates a measurable call/put divergence. The blue dots (calls) and red dots (puts) should overlap — but on the left panel, they're separated by over 2 vol points.

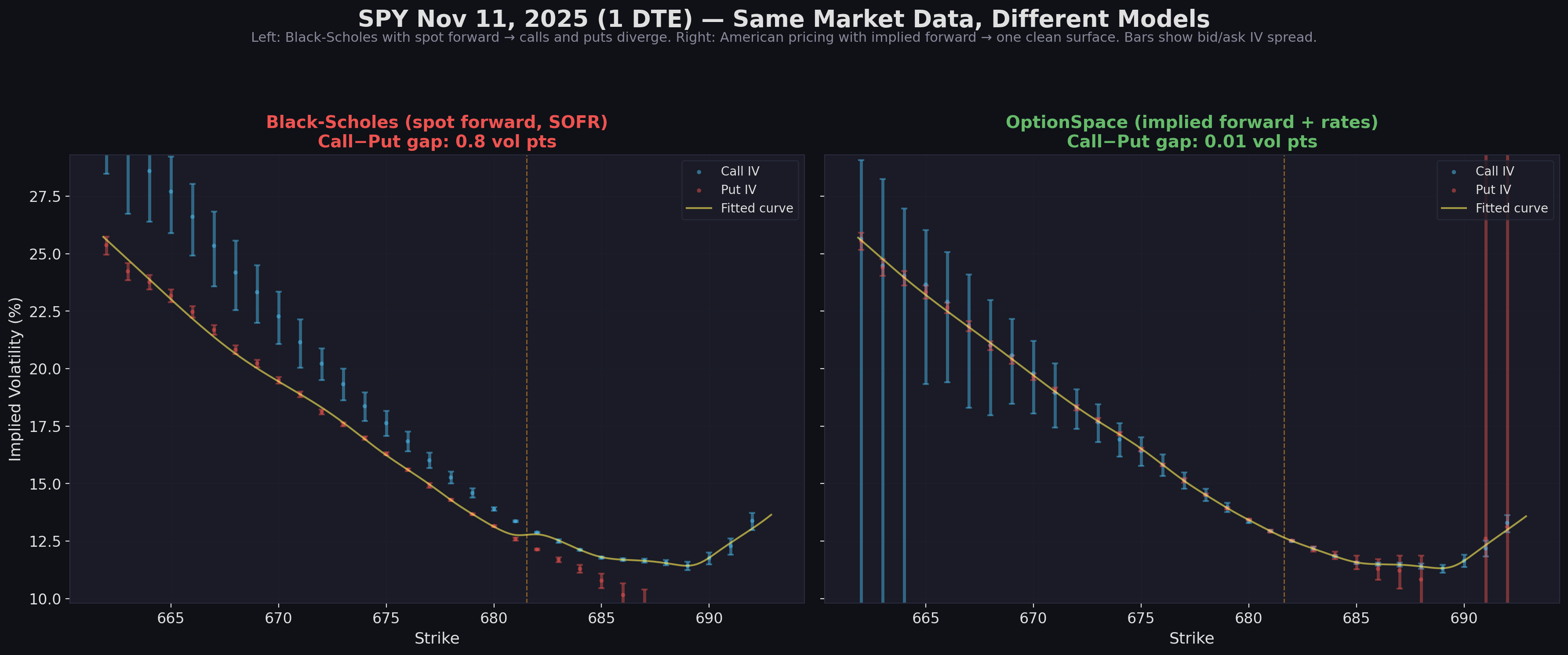

Left: 2.3 vol point gap. The averaged curve compromises between calls and puts — fitting neither correctly.

Right: 0.01 vol point gap. Calls and puts overlap within their bid/ask spread. One clean curve fits both.

Right: 0.01 vol point gap. Calls and puts overlap within their bid/ask spread. One clean curve fits both.